Banking used to be considered a difficult sector to disrupt. Regulation aside, customer inertia proved strong and a personal relationship with the branch manager was all that was needed to secure clients’ custom. Today’s landscape, however, is very different. Consumer banking has led the way in changing customers’ expectations of the banking experience. Usability and convenience are key, as well as mobility – with 63% of people choosing to manage their finances on the go.

Companies that provide consumer banking with this mobility in mind are rapidly garnering significant client bases. Since launching in 2014, online-only bank, Chime, has gathered in 1,000,000 customers and is growing by 100,000 accounts a month. These are not people new to banking – they are coming from other banks, ones that couldn’t respond to their needs.

Related articles to read next:

Collaborative disruption – why fintech is a friend to community banking

The new reality of the financial services sector

Business banking looks set to follow suit. Ultimately, providers of business banking facilities will need to find ways of adapting to a consumerized, digital-first market if they’re to hold onto their client lists. That said, responding to such a sea-change in customer needs is no small ask, and global companies are committing large sums to the project.

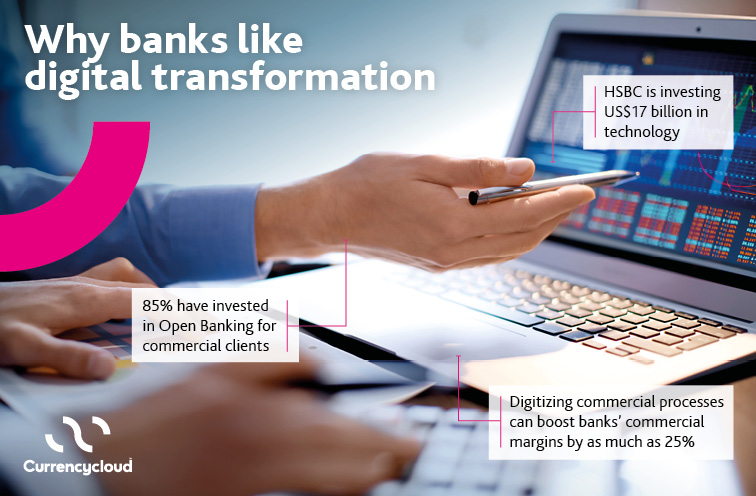

HSBC, for example, plans to invest up to US$17 billion in technology by 2020 to grow its market share with corporate clients. “After a period of restructuring, it is now time for HSBC to get back into growth mode,” said HSBC CEO John Flint.

Fintechs can help smaller banks

It is understandable that a bank with the scale of HSBC would be able to invest tens of millions in a near-term digitization process. For smaller banks, it may not be possible to embed technology to such an extent. The answer is to bring third-parties to the table which helps either fill gaps or scale services rapidly with low-risk commitment and little trauma to existing systems.

Techcrunch reported Naveed Sultan, global head of treasury and trade solutions for Citi, as saying: “If fintech can come and pick up a part of a value chain which we believe they can execute better than us, at better economics and scalability, the banks have inherent incentive to pass that activity on to fintech and move on to the value-added space.” The fact that a global banking player is also choosing to use third parties to expand its capabilities shows that using fintech is a strategic step, rather than a next-best option for cash-strapped companies.

Can we help with your digital transformation?

Click to learn more about Currencycloud’s payment platform technology

Next generation business banking

The market is certainly growing apace. Accenture’s 2018 Open Banking for Businesses found that: “More than 90 percent of banks in our survey see Open Banking for SMEs and large corporations as a key strategic initiative in their digital transformation programs. More than 85 percent have already invested in Open Banking for commercial clients or plan to do so in 2019. Importantly, half of banks expect five to 10 percent of their revenue growth to come from Open Banking.”

Open banking as described in Accenture’s report is just one facet of digital disruption that has transformed customer banking and is making waves for business clients. An Oracle study found that corporate banking customers had a shopping list of features that includes, but is not limited to:

- Customized and superior advisory

- End to end solutions

- Innovative products and services

- Customized solutions

- Price competitiveness

- Transparency

- Superior digital experience

Not being able to provide these solutions is a huge question of opportunity cost to banks. A reporter for Digitalist, for example, claimed attendees at the financial services’ Sibos conference in Toronto in 2018 suggested that the gap between consumer and business banking experience was becoming a deal-breaker:

“Attendees said this gap is a problem. Quite a few told me with no hesitation that the client experience in institutional banking needs to change and evolve. Corporate banks, they argued, need to deliver an optimal digital experience to corporate users, who account for much of each bank’s revenues. The status quo – limited online banking and mobile access – isn’t enough.”

It’s not just an insurance policy against customer defections, although this alone should be reason enough to invest in improving business banking experience. McKinsey estimates that digitizing commercial processes can result in a 25% improvement in commercial banks’ margins, as well as raising customer satisfaction scores.

Friend or foe?

There is a tendency to view the disruption of the business banking marketplace in a combative fashion. There are invaders at the gate, in the form of Challenger Banks and third-party providers. The vocabulary we use here says it all – ‘Challenger’ banks and digital ‘disruption’. If the language focused more on ‘Support’ organizations or ‘Partner’ innovators, the sector might be able to see the real opportunities in this changing sector.

Certainly, most fintechs are the latest word in agile innovation and are able to bring enhanced customer experience, cost-effective solutions and machine learning-driven products for niche customer segments at scale. Responsiveness, in terms of accessing new markets and being able to scale or reduce practically on-demand, is also a clear benefit.

The challenge of regulatory compliance

For many traditional organizations, the opportunity to work with fintechs will not become an either/or option. Regulation around banking and data looks set to intensify with the pace of technological innovation behind many of the changes. Banks don’t just need to try and answer consumer demand for a more digitized customer experience, compliance will drive change that fundamentally impacts their business models.

According to the Oracle study mentioned above: “The current technology systems used by banks are not robust enough to accommodate these changes and meet the regulatory requirements. This can have a serious impact on banks’ bottom-line, making them less competitive.”

Certainly, if traditional providers of business banking make no attempt to move forward with more customer-friendly experiences, they will find themselves on the wrong side of history. Those more willing to adapt and bring on board new ideas will not just be future-proofing their organizations, but they will be opening themselves up to a whole new set of revenue streams.

Find out more about how Currencycloud can help your business.